Form ADV is an SEC filing which all companies managing AUM in excess of $25M need to file annually. Often regarded as one of the most important public disclosures, this form summarises a firm’s business, its ecosystem of clients and products and services.

The nature of the form ensures that the information collected is highly relevant in assessing the operational risk of an investment and the investment manager. A study by Brown et al states that filing Form ADV alone may be a potential signal of the firms’ quality, because of the stringency in filing requirements.

The form is divided into two parts –

- The first part identifies the adviser's business, compliance information, client base, disciplinary matters, and compensation structure

- The second part records an explanation of the advisory services rendered, risks associated with its management style, and other items that may be material to investors and fiduciaries.

The nature of the filing helps understand internal operational risks such as the failure of internal audit, systems and accounting systems, failure of compliance and misconduct. Operational risk events include losses due to rogue traders ( eg Societe Generale), failures due to management fraud (eg Enron) and reputational risks like the 2004 mutual fund scandal (Putnam) etc. (Brown et al).

It is often assumed that market risks can be measured using quantitative risk models while operational risk has no direct numerical proxy, therefore it relies on intangible variables. However, Form ADV mandates various operational risk disclosures which can be translated into quantitative variables, that can further be used in risk models. Due Diligence is possible by the analysis of the qualitative data provided via Form ADV. You can access Form ADV information and translated risk scores of firms on RADiENT via the Advisers tab!

We would now break the form into major categorical heads, to understand the kind of information a user can extract from Form ADV to carry out the due diligence process.

ORGANISATION DETAILS

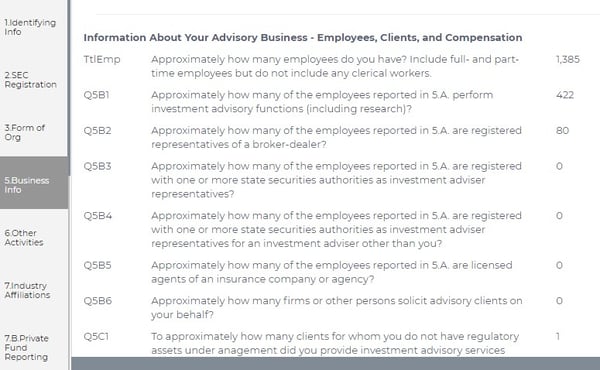

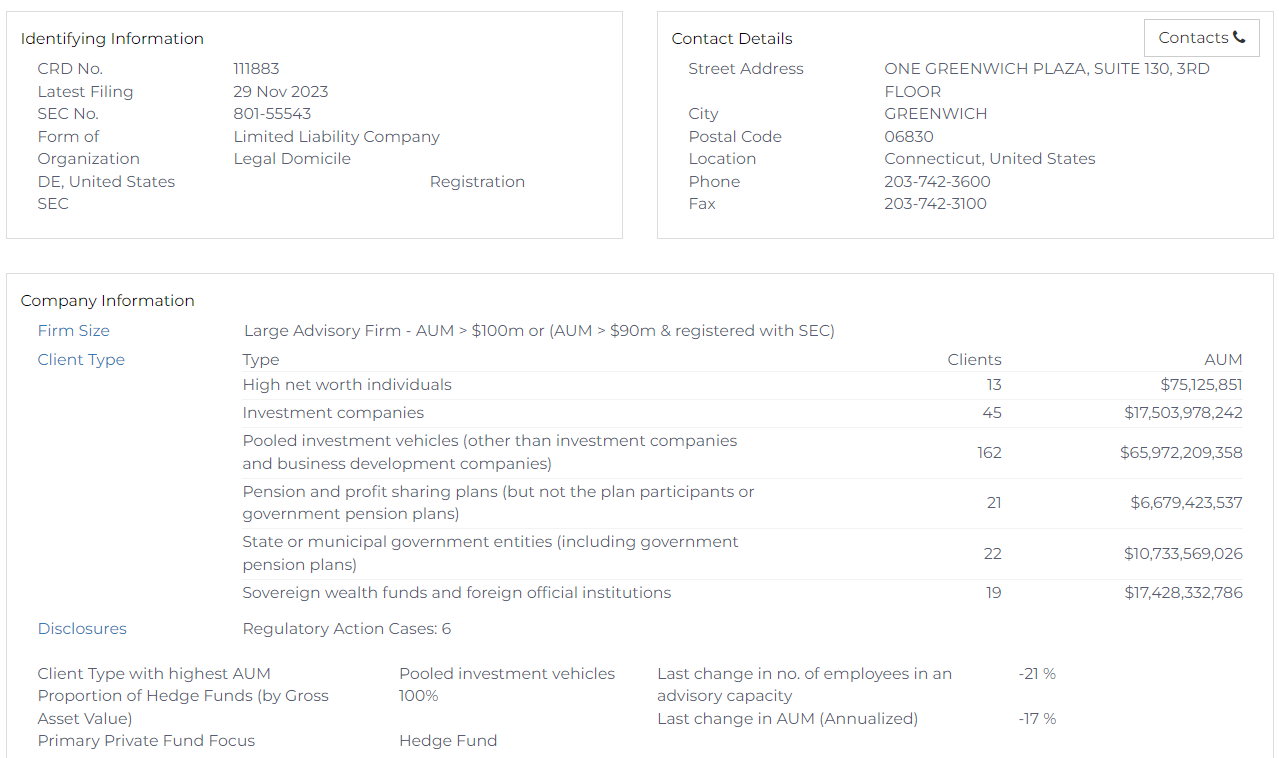

Basic information about the business- its legal structure, asset size, employees, types of advisory activities etc. Changes in the firms' assets, clients and other factors over time may reflect whether the business is unexpectedly growing, shrinking, or evolving.

Form ADV requires entities to disclose information about the compensation of their advisory services. The firms provide detailed information about the fees and expenses that the clients are subject to, like- if the company deducts fees from the clients’ assets or if the clients are subject to paying extra amounts in connection to the firm’s advisory services such as custodians’ fees or mutual fund expenses. Additionally, the form also records how the firm is compensated for its services, i.e. if the compensation is performance-based, time-based, is a subscription or a fixed fee etc.

The firm's compensation structure could help understand whether agency risks or alignment of interests may be an important motivator or distraction for the firm’s employees. Compensation paid to the firm by sources other than clients and the financial relationships with third-party marketers is disclosed to further facilitate a deeper understanding of the firm’s activities.

Investors can analyse the industrial reputation of the funds/firm’s brokers, custodians, auditors and brokers etc which are required to be disclosed in Schedule D. They can also look for possible inconsistencies in the firms functioning by checking for the replacement of these service providers and their tenure with the firm.

COMPLIANCE

The form records information about the firms’ CCO. The SEC states that a CCO ( Chief Compliance Officer) should be “competent and knowledgeable regarding the Advisers Act and should be empowered with full responsibility and authority to develop and enforce appropriate policies and procedures for the firm.”

If the CCO’s role is outsourced to an outside firm, the disclosure of information should prompt the investor to further research into the scope and manner of the adviser’s compliance process.

RADiENT facilitates CCO search across the spectrum of ADV filings, so you can gauge the CCO's experience and reputation.

DISCIPLINARY DISCLOSURES

Form ADV requires past details on the personnel such as past criminal charges, including the nature, severity and disposition of the past charges. This disclosure enables the investors to further analyse whether the organization’s actions are undermining its words of integrity or aligned interest on behalf of clients.

Past performance can be considered a viable indicator when assessing the functioning of the firm. “Past manager behaviour may include previous fiduciary decisions, as well as previous legal and regulatory actions taken against the manager or any other variable that could be correlated with the propensity to make future illegal or unethical decisions.”

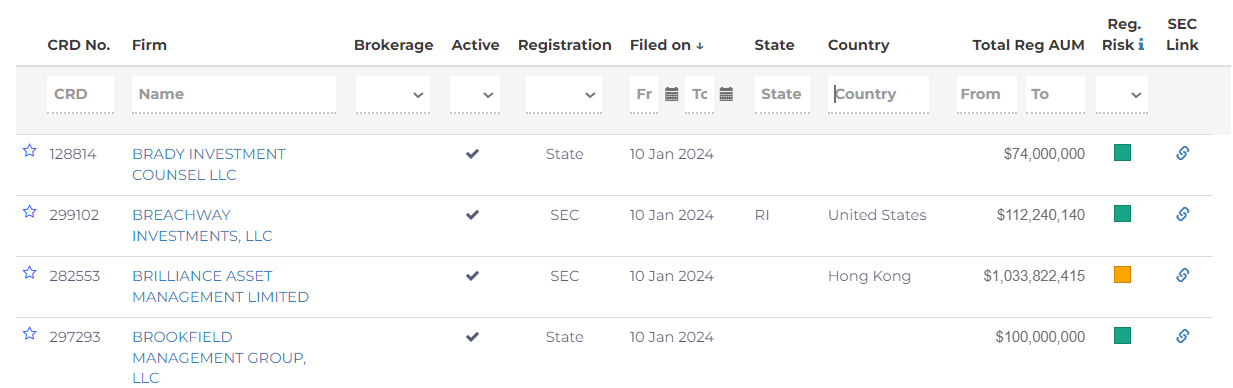

RADiENT extracts disclosure information pertaining to the disciplinary history of the firms and their advisory affiliates from item 11 of the ADV filings. This data is then presented to the users on the Advisers tab with a clear indication of the firms’ regulatory actions using colored tiles.

The green-colored tile (low) indicates that the entity has no regulatory/ civil/ criminal disclosures of the last date of filing. The yellow tile (medium) indicates that some questions, except those relating to felony /misdemeanour charges/convictions, were answered in favor of possibly risky actions. The red tile (high) indicates that the entity has recognised its actions and is being charged with / convicted of a felony/misdemeanour.

The filing records specific details of each client type, the dollar amount of assets under management, including an overall percentage exposure to non-U.S. clients. These additional details help enable a more precise metric to monitor. The relative and absolute change over time in these numbers can indicate the health and direction of that adviser’s business development and its aligned interests.

Registered AUM and client information can also disclose information about the adviser's retention trends and client development.

CLIENT-BASED INFORMATION

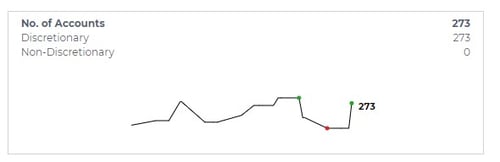

Form ADV also records information on the Discretionary and Non-Discretionary accounts held by an entity. This could help investors make informed assumptions about the faith other investors have in the entity’s investment decisions. A higher number of Non-Discretionary accounts may indicate wariness amongst the investors in relation to the entity's investment decisions.

The filing provides insights into the client type and their affiliated AUM. This information can assist investors in evaluating the popularity of the firm and the preferences of other investors. Client type is also a good indicator to understand a firm’s sources of cash flow.

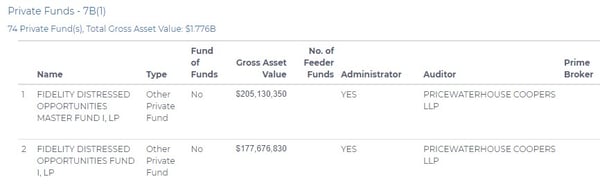

PRIVATE FUNDS

Section 7B-1 of Schedule D records in-depth details of its private funds and the advisory services provided to this fund. Fund information disclosed in Section 7B-1 includes details about :

- If the fund is a ‘Master Fund’

- If the fund is a ‘Fund of Funds’

- If the fund is a ‘Feeder Fund’

- Census type information of the fund affiliates

- Ownership details and Minimum investment required by investors etc

Investors can use this information to gauge a sense of the operational activities of the fund, they can search for whether the entity is a subadvisor for a fund. Information on the sub-advisory services of the company can help investors make well-informed investment decisions, for sub-advisers are known for their investment style, expertise and track record in a specific investment strategy.

Detailed disclosures on hedge funds, alternative funds and other unregistered pooled investment vehicles provide various insights about funds’ assets with other sources. Investors can also gauge information on how much private fund assets are owned by related persons of the adviser. This can help understand the motivation behind the performance of related private funds and the advisers' involvement.

Just as investors can review their managers' profiles using Form ADV, this form can be leveraged by specific firms and their managers to review their peers’ ADV profiles. Additionally, Form ADV can also provide insights on :

- New funds launched

- New emerging markets

- Market intelligence

- Turnover related changes

- New manager relations

- Potential M&A activity

The end goal of Form ADV is to enable investors to make informed decisions in which all material facts are consistently and appropriately considered. RADiENT further simplifies the due diligence process for its users by integrating information from other filings such as Form NCEN, Form NPORT, Form 13F etc. You can access this data in user-friendly and easy to read formats, by simply signing up with RADiENT!

i) Form ADVs: Dragnets of Due Diligence, Callan Institute, 2018

ii) https://www.fischerfinancialservices.com/due-diligence/

iii) Brown et al, Mandatory Disclosure and Operational Risk: Evidence from Hedge Fund Registration, Journal of Finance, Wiley, 2008.